ZIMMER BIOMET HOLDINGS (ZBH)·Q4 2025 Earnings Summary

Zimmer Biomet Beats Q4 on Revenue & EPS; Guides Cautiously for 2026 Sales Transition

February 10, 2026 · by Fintool AI Agent

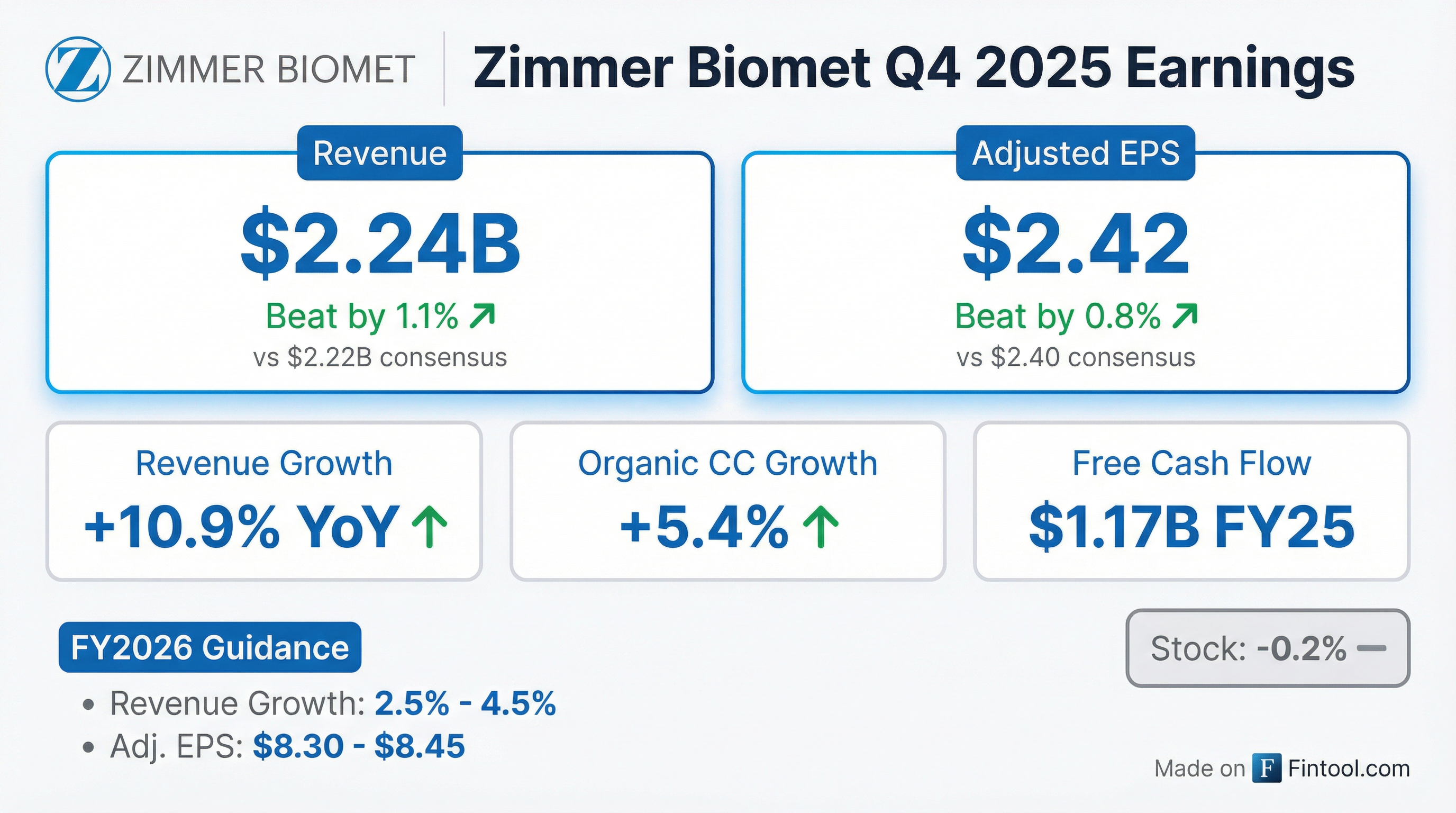

Zimmer Biomet delivered a solid Q4 2025, beating both revenue and EPS consensus while guiding cautiously for 2026 as the company transitions its US sales organization to a predominantly direct model. Net sales of $2.24B grew 10.9% YoY (+5.4% organic constant currency), while adjusted EPS of $2.42 rose 4.8% YoY.

The stock rallied +5.6% following the earnings call, as investors responded positively to CEO Ivan Tornos's detailed breakdown of the sales transformation rationale and timeline, despite the conservative 2026 guidance range of 1-3% organic growth.

Did Zimmer Biomet Beat Earnings?

Yes. Zimmer Biomet beat on both top and bottom line metrics:

This marks ZBH's eighth consecutive quarter of EPS beats. The company's trailing four-quarter average EPS surprise is approximately 2.2%.

Revenue growth breakdown:

The gap between reported and organic growth reflects the Paragon 28 acquisition (completed April 2025), which added ~380 bps to growth.

What Did Management Guide for 2026?

Management issued 2026 guidance that reflects near-term headwinds from the US sales transformation:

The organic revenue guidance of 1-3% represents a deceleration from FY2025's 3.9% organic growth, as the company invests in transforming its US sales organization from a largely independent agent model to a direct, specialized sales force.

CEO Ivan Tornos acknowledged the trade-off: "While this bold action tempers our 2026 sales guidance, we are confident that it will drive durable long-term growth and solidify our position as the undisputed market leader."

EPS guidance of $8.30-$8.45 represents 1-3% growth vs FY2025's $8.20, signaling margin discipline despite the sales transition costs.

Operating margin phasing for 2026:

- Q1: Down ~100 bps YoY (Paragon 28 not yet anniversaried, higher commercial investments, lower gross margin)

- Q2: Up ~100 bps sequentially as Paragon 28 anniversaries

- H2: Roughly in line with 2025 levels

Management expects gross margins of 70-71% for full-year 2026 (vs. 72.4% in Q4 2025), offset partially by SG&A efficiencies.

How Did the Stock React?

ZBH shares rallied following the earnings call, trading up +5.6% to $94.80 as investors responded positively to management's detailed execution plan for the sales transformation.

Key context:

- 52-week high: $114.44

- 52-week low: $84.59

- Current price: $94.80 (up from $89.73 pre-call)

- Today's range: $91.26 - $95.13

- 50-day moving average: $90.46

- 200-day moving average: $95.34

The positive reaction suggests investors appreciated CEO Ivan Tornos's detailed explanation of the sales transformation rationale and timeline, combined with the beat on Q4 numbers and strong free cash flow trajectory.

What Changed From Last Quarter?

Revenue momentum accelerated. Q4 marked the second consecutive quarter of mid-single digit organic growth after multiple quarters of ~2-3% organic growth in early 2025.

*Values retrieved from S&P Global

Segment performance highlights:

*S.E.T. = Sports Medicine, Extremities, Trauma, Craniomaxillofacial, Thoracic; includes Paragon 28 acquisition impact (+15.8 ppts)

Within S.E.T., CMFT and Upper Extremities continue to perform strongly (mid-teens and high single-digit growth respectively), while management acknowledged trauma and restorative therapies (HA injections) remain "problem children" and headwinds.

Knees showed notable strength with 6.0% US growth and 8.2% international organic growth. Key drivers included:

- Persona OsseoTi (total cementless knee) reached ~35% penetration, with rapid ASC adoption

- Oxford Partial Cementless continues to outperform expectations with high conversion rates from competitive accounts

- Direct-to-patient campaign with Arnold Schwarzenegger ("personalized knee") yielded meaningful results in H2

Hips delivered nearly 8% US growth, driven by the Z1 triple taper stem now at 35% of US hip stems with "meaningful competitive conversions."

Robotics & Technology grew over 10% in the US during Q4 — the strongest robotic capital sales quarter in over 2 years.

Key Management Commentary

On the US sales transformation:

"We are excited about our transition to a predominantly direct and specialized sales organization in the U.S." — Ivan Tornos, CEO

On capital allocation: The Board authorized a new $1.5 billion stock repurchase program commencing February 9, 2026, with no expiration date. This follows $250M in Q4 repurchases and $487M for FY2025.

On innovation pipeline: Management highlighted several recent wins:

- FDA clearance for ROSA Knee with OptimiZe — the most significant upgrade to the robotic knee platform since its 2019 launch

- World's first iodine-treated hip procedure in Japan using iTaperloc Complete system

- Launched Brachiator Mini-Rail External Fixation System through Paragon 28

Full-Year 2025 Performance

The GAAP EPS decline reflects elevated restructuring charges ($181M in FY2025 vs $219M in FY2024), acquisition-related expenses ($77M), and inventory charges related to product line discontinuations ($206M).

Capital Allocation & Balance Sheet

Debt increased ~$1.3B YoY primarily to fund the Paragon 28 acquisition ($1.39B in acquisition-related cash outflows).

FY2025 Capital Returns:

- Dividends: $190.3M

- Share Repurchases: $487.0M

- Total Returns: $677.3M (~58% of free cash flow)

Risks and Concerns

1. US Sales Transformation Risk — The shift from independent agents to direct sales is the largest change to ZBH's go-to-market model in decades. Management acknowledged this "tempers" 2026 guidance, and execution risk remains elevated.

2. Elevated Debt Load — Net debt of ~$6.9B and recent senior note issuances put leverage at elevated levels following the Paragon 28 acquisition.

3. Product Discontinuation Costs — The company recorded $162M in excess and obsolete inventory charges in Q4 alone related to product lines it intends to discontinue by 2032.

4. Tariff Exposure — Management cited "navigating tariff headwinds" as a 2025 challenge, suggesting ongoing macro uncertainty.

5. Restructuring Continues — Multiple active restructuring programs (initiated December 2019, 2021, 2023, and February/December 2025) indicate the transformation is ongoing.

Q&A Highlights: What Did Analysts Ask?

The Q&A session focused heavily on the US sales transformation. Key exchanges:

On the sales transformation rationale (Matt Blackman, TD Cowen): CEO Ivan Tornos explained the "what, why, how, when" of the transformation:

"We're moving from being a company... that has a lot of non-dedicated employees. We got people that have two, three jobs while working at Zimmer Biomet... Our productivity rates in the U.S... are roughly half of what some of our direct competitors have."

The company has ~2,500 reps across 34 territories, with one-third of the transition already complete. Expected completion: end of 2027.

On what's embedded in guidance (Rick Weiss, Stifel): Tornos outlined three focus areas: (1) US sales force transition execution, (2) new product adoption rates for the "Magnificent Seven" platform, and (3) international performance in key geographies.

On pricing outlook (Patrick Wood, Morgan Stanley): CFO Suky Upadhyay explained the expected step-down from flat pricing in 2025 to up to 100 bps erosion in 2026, driven by EMEA price moderation, Japan's biannual price decrease, and China go-to-market reconfiguration.

On gross margins (Matt Taylor, Jefferies): Upadhyay guided gross margins of 70-71% for 2026 (down from 72.4% in Q4 2025), with drivers including lower volume leverage, FX hedge gains tapering, and price/mix headwinds. More than half is expected to be offset through SG&A efficiencies.

On Q4 strength (Robbie Marcus, JPMorgan): Management confirmed Q4 outperformance was driven by new product acceleration, with modest benefit from capital sales and ASC purchases. International knee growth of 8.2% included some Middle East revenue that slipped from Q3.

On capital allocation (Larry Biegelsen, Wells Fargo): Tornos characterized the shift toward buybacks as a "pause" rather than a change: "We've done three acquisitions between OrthoGrid, Paragon 28, and Monogram... This is not the time to add more complexity." The company approved a new $1.5B buyback authorization and plans to prioritize returns over M&A in 2026.

On ASC penetration (Caitlin Cronin, Canaccord): ZBH ended 2025 with 20-22% of US hips and knees performed in ambulatory surgical centers. Management expects Monogram robotics to accelerate ASC adoption given its speed, efficiency, and accuracy advantages.

On mBOS/robotics (Joanne Wuensch, Citibank): The mBOS autonomous robotic system from the Monogram acquisition will be the "main event" at the AAOS Academy meeting in New Orleans. Tornos described it as "definitely the step of moving from guided robotics to smart robotics" with best-in-class ease of use and registration speed.

On knee strength internationally (Matt Miksic, Barclays): International knee growth of 8.2% was driven by Oxford Partial Cementless (the only FDA-approved partial cementless knee), Persona OsseoTi at ~35% penetration, and the Persona Revision launch in Europe. The iodine-coated device launch in Japan (Q1 2026) offers a 40% price uplift vs. non-iodine products.

Forward Catalysts

- AAOS Academy Meeting (New Orleans) — mBOS autonomous robotic system debut; management calls it the "main event"

- Q1 2026 results (expected early May) — First look at sales transformation impact and iodine-coated device adoption in Japan

- ROSA Knee with OptimiZe adoption metrics — Key driver of knee share gains

- Paragon 28 integration — One-year anniversary in April 2026; management committed to double-digit growth

- Share repurchase activity — New $1.5B authorization provides floor support; expect 194-195M shares outstanding by year-end

- 2027 outlook — Sales transformation expected to complete by end of 2027, enabling "durable mid-single-digit-plus growth"